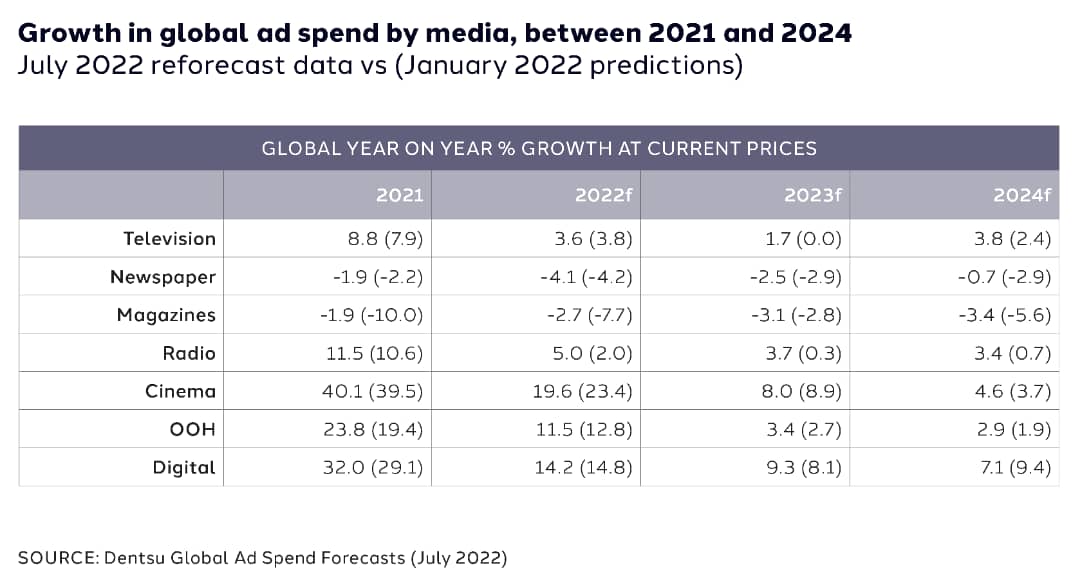

‘holidays’ season for the first time, puts a big retail focus on Q4 and pushes Television ad spend growth to 3.6%, reaching US$192.8 billion. Within this Linear TV is growing by 2.0%, Connected TV (CTV) up by 22.3% and Broadcaster Video on Demand (BVOD) growing by 16.0% as audiences shift to digital platforms.

Out-of-Home (OOH) and cinema will both see encouraging double-digit growth in 2022 (respectively 11.5% and 19.6%). Radio is also forecast to grow, much faster than initially considered with a new reforecast of 5.0% for the year, up from 2.0% in the January predictions – which is mainly due to faster return to office working. As with previous predictions, ad spend in newspapers and magazines will continue to decline.

In 2022, the Americas will be the top ad spend region at US$329.6 billion and the most dynamic with spend increasing by 13.1%. India at 16.0% growth will stay ahead of the US at 12.8% and Brazil at 9.0% as the fastest growing market.

Industry wise, the greatest growth is forecast for the Technology sector (+11.3%), which has benefited from people’s greater reliance on digital devices. Retail is one of the key sectors of spend growth at a rate of 11.0% in 2022. The sector is driven by a number of factors including the significant growth of e-commerce, the entry of new players, and the introduction of emerging retail platforms.

This dentsu Global Ad Spend Forecast not only looks at the data from 58 markets, but also examines some of the key factors impacting ad spend shift, such as inflation increases, sustainability regulation, acceleration of gaming as an ad medium, doubling down on addressable media and also the importance of buying attention as core metric.